LeoPatrizi/E+ via Getty Images

In October 2023, I covered Honeywell and assigned a hold rating to the stock. The stock returned 20.2% compared to 29.3% for the S&P 500. So, a hold rating in my view has been fair. Honeywell will be reporting earnings on the July 25 and in this report, I want to quickly provide an earnings preview before shifting my focus on the recent M&A momentum and valuation of Honeywell stock.

What Are Analysts Expecting For The Second Quarter Earnings?

For the second quarter, analysts expect between $9.3 billion and $9.47 billion in revenues with a mid-point estimate of $9.42 billion providing 3% growth. The reason sales growth is not extremely high is because the comp is becoming more challenging and some business segments are not expected to perform as strongly. One example is the PPE unit that surged during the pandemic but is now not performing as strongly and Honeywell is even exploring selling the unit that would be valued in excess of $2 billion. Similarly, warehouse automation solutions are also seeing off-peak demand. So, revenue growth is not as straightforward as one would think also because production increases in the airplane manufacturing industry are under pressure.

Estimates for earnings per share for Honeywell are expected to be $2.41 at the mid point indicating 8.1% growth with an EPS range of $2.29 to $2.45. It should be noted that to some extent the growth is driven by share repurchases. Over the past two years, Honeywell has beaten estimates on EPS every quarter while it missed revenue estimates five times and beat estimates three times. So, on EPS the track record is stronger than on top line.

Honeywell Acquisitions In Support Of Three Megatrends

In 2023, Honeywell announced that it would be realigning its portfolio with three megatrends. These trends are future of aviation, energy transition and automation. Looking at that realignment, it also makes sense that the company is exploring the sell of its PPE business. However, more importantly we see that there are acquisitions that align with the three megatrends.

In June 2023, Honeywell completed the acquisition of Compressor Controls Corporation for a cash consideration of $673 million and in August 2023 the company acquired SCADAfense which provides cybersecurity solutions. In December 2023, there was a big acquisition as Honeywell acquired Carrier Global Corporation’s Global Access Solutions business for $4.95 billion. The transaction was finalized in June 2024 and was also included in the guidance update for 2024 results. The acquired business will report as part of the Building Automation segment.

In March 2024, there was an acquisition intention announced to strengthen the Aerospace Technologies business with additional autonomous capabilities via a $200 million acquisition of Civitanavi. Against expected EBITDA for 2024, it would imply 12.35x EBITDA.

In June 2024, there was the agreement to acquire CAES Systems Holdings for $1.9 billion valuing the company at 14x estimated 2024 EBITDA. The acquisition allows Honeywell to enhance its defense portfolio.

The latest acquisition is that of Air Product’s Liquefied Natural Gas Process technology and equipment for 13x 2024 EBITDA or $1.81 billion. This obviously feathers into the energy transition megatrend. Whether it is a good acquisition remains to be seen. LNG looks promising, but I believe that the entire process of liquifying the gas is an energy consuming process and that could also explain why Air Products is focusing on energy transition via scaling green hydrogen production.

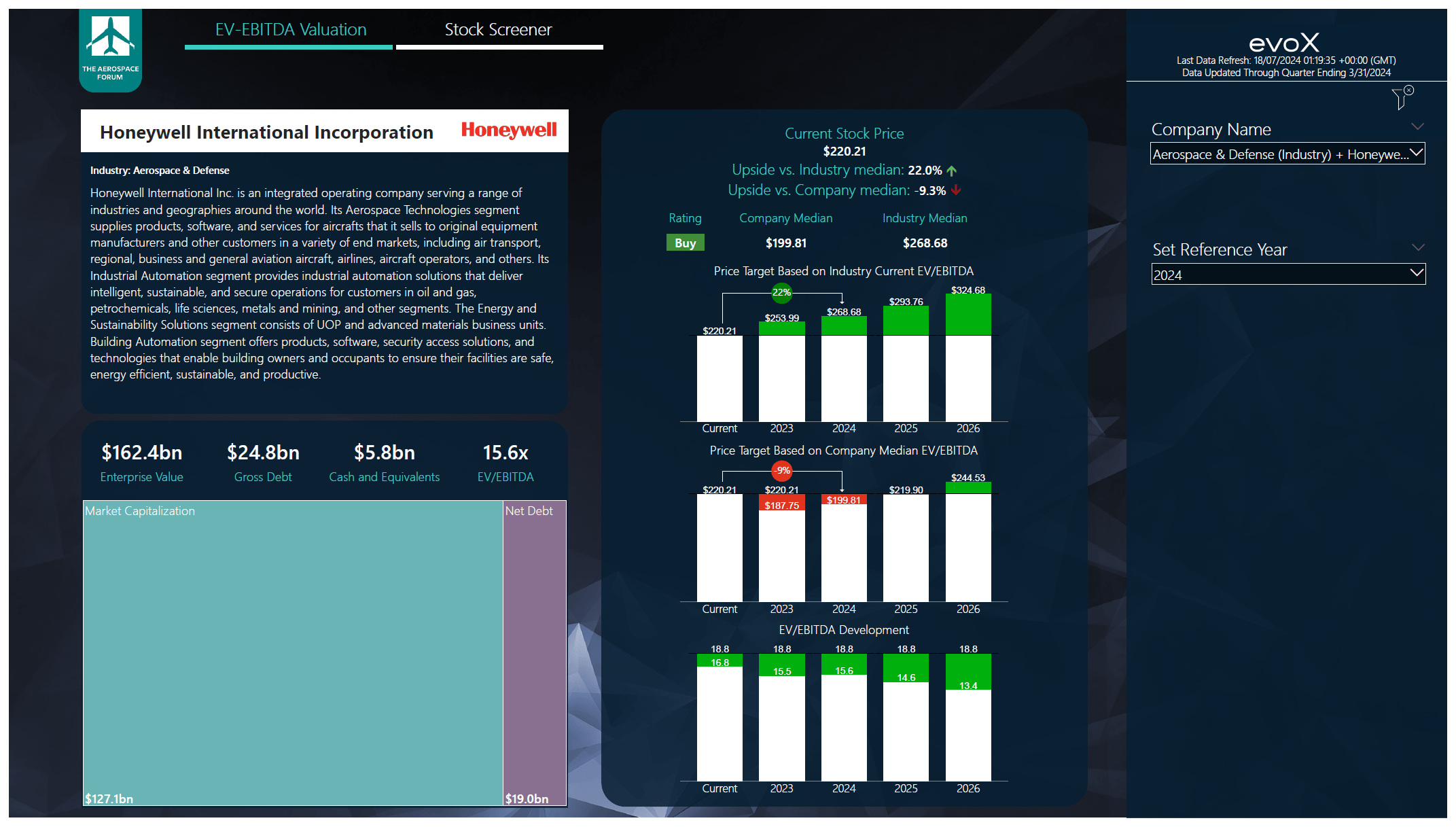

What Is Honeywell Stock Worth?

The Aerospace Forum

With all the acquisitions, it can be a bit of a challenge to value Honeywell stock. There are a few reasons for that, the first one is that we don’t know what assets and liabilities Honeywell brings on the books with the acquisition and because the timing of the transactions is not known we don’t know the contributions and the timing of the cash outflow to acquire the business. However, I am assuming the Civitanavia acquisition to add to the results for at least one quarter this year and for the CAES and LNG acquisitions to be finalized next year.

Compared to my previous report, EBITDA estimates have increased by 2.7% between 2023 and 2025. Against the company’s median EV/EBITDA, the stock seems to be fairly valued with 2025 earnings in mind. So, Honeywell is not a name which I think you should buy because it is discounted, looking at its median EV/EBITDA it is clearly not discounted. However, against the median EV/EBITDA and 2026 projections, there is already 11% upside and if we were to allow some margin expansion against 2024 earnings, we get to a $234 target representing 6% upside. That is not a huge upside, but I believe that the ongoing acquisitions and the focus on three key trends is going to pay off and I think this is a stock to buy and hold for the longer term.

Conclusion: Honeywell Stock Is A Solid Stock To Own

From a valuation perspective, Honeywell stock is not a screaming buy. Against the current year earnings it is 9% overvalued and fairly valued for 2025 earnings. So, that is not something that screams “buy” to me. If Honeywell stock drops more than 9% then it most definitely becomes a stronger buy. The reason why I have assigned a buy rating rather than a hold rating is because there is still upside to the peer group valuation and the key topics around which Honeywell builds its business and acquisitions, namely aerospace, energy transition and automation are trends that will drive business for years if not decades to come. So, this is not a stock that I view through a short-term lens.