Chris Hondros/Hulton Archive via Getty Images

Celsius: Feeling The Heat Of A Bear Market Decline

Celsius Holdings, Inc. (NASDAQ:CELH) investors have endured a massive hammering since CELH topped out again below the $100 level in late May 2024. As a result, while my upgrade to Celsius stock seemed timely, the market has proved me wrong since then. I anticipated a buy-the-dip opportunity, even though I acknowledged its valuation was still expensive. As a reminder, I had previously cautioned investors with a Sell rating on CELH in February 2024. I underscored its highly expensive valuation and assessed that its global expansion plans weren’t sufficient to justify the market’s bullishness.

As a result, I must admit that the stock’s volatility has dumbfounded me, suggesting that the market has finally focused on Celsius stock’s aggressive valuation.

Celsius: Disappointment Must Be Reversed

The stock was hit by selling intensity after CELH’s Q1 earnings release. The lifestyle energy drink leader’s results missed estimates as the market reacted to tough comps. In addition, inventory adjustments by PepsiCo (PEP) also worried investors, given PepsiCo’s significant contribution (62%) to Celsius’ North American business in the first quarter.

Despite that, Celsius is confident that PEP’s inventory adjustments are assessed to be “noise,” causing volatility in the company’s “sequential quarterly revenue figures.” Furthermore, the energy drinks leader telegraphed that underlying demand has remained stable, demonstrated by the high ACV of 98.4%.

Celsius has continued to gain market share against its leading peers, underscoring its robust execution. Consequently, I assess that the market has likely reflected higher execution risks in the second half, as PEP’s recent Q2 performance disappointed. PepsiCo faced weaker sales in Q2, likely attributed to “declining consumer purchasing interest.” As a result, the market leader may need to reduce its prices as “consumers are becoming more price-conscious and looking for value.”

Therefore, recent Nielsen retail channel data showing a “sequential slowdown” in Celsius’ YoY sales growth has increased the execution risks on its ability to deliver. Heightened concerns about “an increase in promotional rates and a slight loss of market share” have weighed on CELH’s buying sentiments, as the stock isn’t priced for disappointment.

CELH Isn’t Priced At A Discount

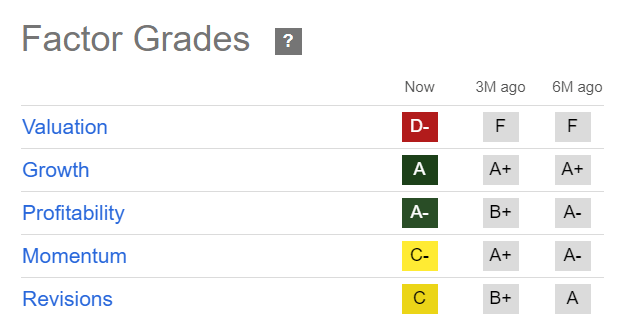

CELH Quant Grades (Seeking Alpha )

The stock is still priced at a steep premium, as seen with its “D-” valuation grade. While it’s much lower than the “F” grade assessed over the past six months, it’s by no means cheap.

CELH’s forward adjusted EBITDA multiple of 31.9x is significantly above its sector median of 10.6x. Furthermore, it’s also well over its beverages peers’ median of 17x (based on S&P Cap IQ data). Therefore, the market has likely downgraded CELH’s growth prospects, as seen with recent downward revisions in the company’s estimates.

Celsius bulls will likely point out that the company is still early in its global expansion plans. Moreover, it has also demonstrated its ability to gain more share against the market leaders in the US market. Celsius’ partnership with PEP has increased its exposure in the food service channel. In addition, its ability to garner a 20% share in Amazon (AMZN) should justify the market’s optimism.

Therefore, the intense battle between the bulls and the bears is likely in assessing its growth valuation, suggesting further near-term volatility must be anticipated.

Is CELH Stock A Buy, Sell, Or Hold?

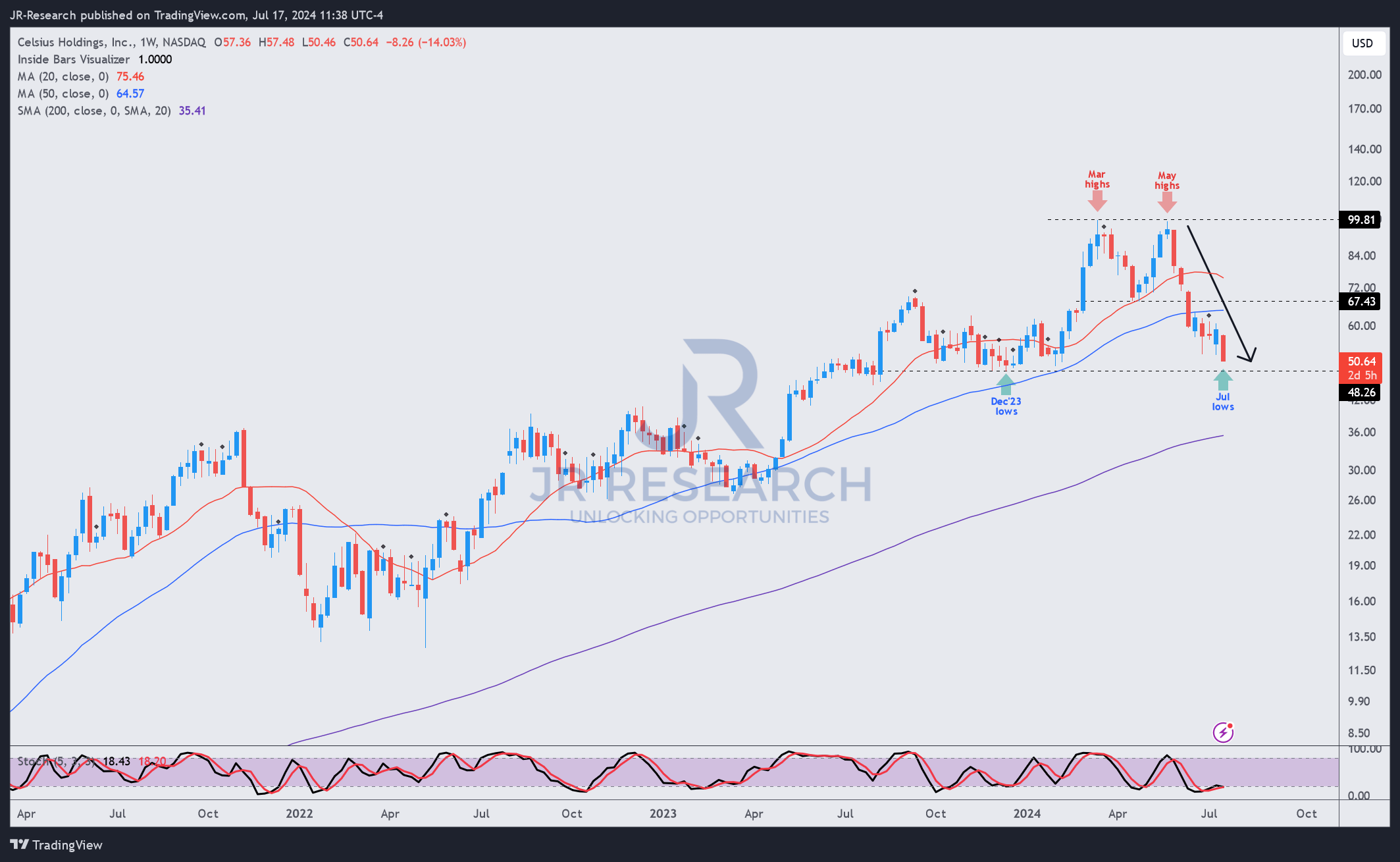

CELH price chart (weekly, medium-term) (TradingView)

CELH’s price action suggests a steep selloff from its March 2024 highs below the $100 zone. Therefore, it’s assessed as a high-conviction sell level for investors who likely took profit. As a result, investors are urged to abstain from adding too close to that level until a decisive breakout higher is ascertained.

With CELH dropping closer to its December 2023 lows, I expect it to attract more aggressively dip-buying sentiments. It’s crucial to note that the stock has remained in a medium-term uptrend despite its bear market decline.

Robust buying support has also been assessed above the $48 level, defended stoutly since late 2023, underpinning my buying conviction. The stock’s “C-” momentum corroborates the lack of panic selling, which could have led to an even steeper plunge.

Notwithstanding my optimism, investors must be prepared for further near-term downside, potentially re-testing the $48 level. Therefore, Celsius must arrest a further drop in sequential YoY growth rates over the next year as the market digested its expensive growth premium.

Given the assessed slowdown in its core US market, the company’s execution in global markets in the second half will be scrutinized. While a more robust global expansion phase could drive a valuation re-rating, CELH isn’t priced for disappointment. Hence, growth-oriented investors mustn’t throw caution to the wind. If the $48 level fails to hold decisively, I assess that a steeper decline toward the $26 level is also possible, although that isn’t my base case for now.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!